Living in Hawaii has its own rhythm — sun, surf, and yes, the occasional curveball from nature. One thing that often catches people off guard is how flood zones and FEMA maps affect real estate, insurance, and long-term planning here. Whether you’re already living in Hawaii or planning a move, understanding flood risk isn’t optional — it’s essential.

In this guide, we’ll break down how to check flood zones, what FEMA’s Risk Rating 2.0 actually means in 2025, and why your monthly insurance premiums might look different than they used to. No fluff — just the facts you need, to understand your risk and potential expense.

How to Check Flood Zones in Hawaii

Before you get too far into house hunting or building plans, it’s worth knowing how to check your flood zone — and how to interpret what you find.

Start with FEMA’s Flood Map Service Center

The official site lets you search by address and pull up your property’s Flood Insurance Rate Map (FIRM). You’ll see zones labeled as A, AE, VE, X, etc. Quick breakdown:

-

Zone AE or VE: High-risk, coastal or near-stream areas — flood insurance typically required by lenders.

-

Zone X (unshaded): Considered low-risk — but that doesn’t mean no risk.

Sometimes it’s not all rainbows in Hawaii.

Raindrops by racruth is licensed under CC0 1.0. Image may have been resized or cropped from original.

County-Specific GIS Tools

Each Hawaii county also has its own GIS (Geographic Information System) portal with interactive flood layers. These tend to be more detailed and up to date. For example:

-

Honolulu County has a robust DPP GIS portal.

-

Hawaii County (Big Island) offers zoning overlays that include tsunami evacuation and lava flow zones too — helpful context beyond just FEMA data.

Real Talk: FEMA Maps Aren’t Perfect

Maps can be outdated, especially in rapidly changing coastal or lowland areas. A property not in a mapped high-risk zone today could still experience flooding in heavy rain events or king tides.

What Is FEMA’s Risk Rating 2.0 — and Why It Matters in 2025

As of 2025, Risk Rating 2.0 is no longer “new” — but many people still misunderstand it. FEMA overhauled its National Flood Insurance Program (NFIP) pricing model to make premiums more equitable and reflective of actual risk.

Here’s what’s changed (and still confusing folks):

1. Individualized Risk Pricing

Under Risk Rating 2.0, flood insurance rates are no longer based solely on flood zones. Instead, FEMA looks at:

-

Distance to water sources

-

Elevation of the home

-

Construction type and foundation

-

Cost to rebuild

Two homes in the same zone could now have very different premiums.

2. Monthly Payment Options

One win for homeowners: You can now pay your NFIP premium monthly instead of upfront. In 2025, this option is rolling out more widely through the NFIP Direct system and approved private insurers — giving a bit more breathing room to those on a tight budget.

3. Rate Caps Still Apply (Sort Of)

FEMA still limits annual rate increases to 18% for primary residences. That helps — but if you’re just now entering the program, don’t be shocked if your “intro” rate is higher than you expected.

Understanding Hawaii’s Special Flood Hazard Areas (SFHAs)

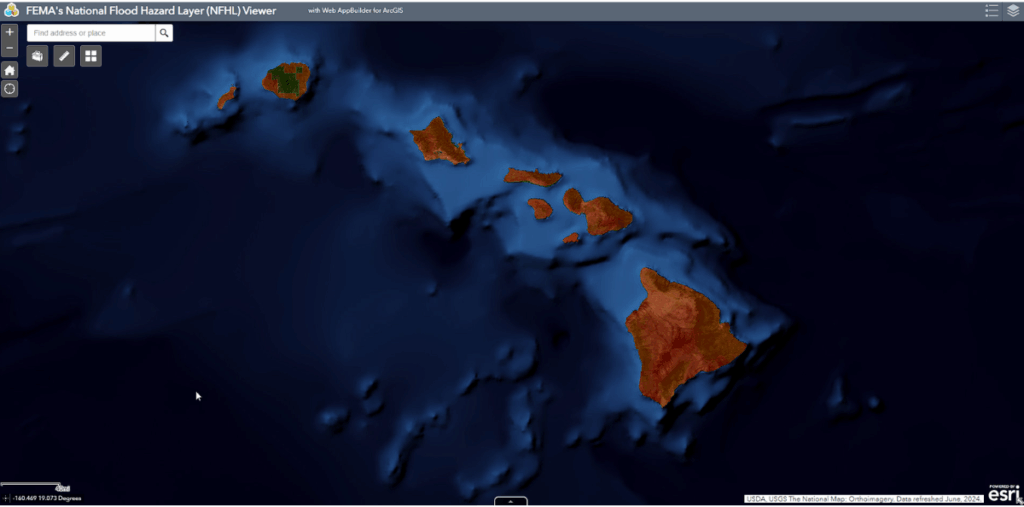

Zoomed out FEMA flood zone map for Hawaii

In Hawaii, Special Flood Hazard Areas (SFHAs) are the zones where FEMA has determined there’s at least a 1% annual chance of flooding — aka the “100-year flood.” If your property sits in one of these, there are real implications for both building and insuring.

What Zones Count as SFHA?

Generally, Zones A, AE, AH, AO, and VE are considered high-risk SFHAs. Here’s what they mean in Hawaii’s context:

-

Zone VE (Velocity Zone): Typically along open coastlines where storm surge and wave action are expected. Common in low-lying parts of Maui and Kauai.

-

Zone AE: Found in flatter areas near rivers and streams, including spots on Oahu’s windward side and pockets of the Big Island.

-

Zone AH & AO: Often tied to shallow flooding in alluvial areas or flatter terrain during intense rainfall.

If your property falls in one of these zones and you have a federally backed mortgage, flood insurance is mandatory.

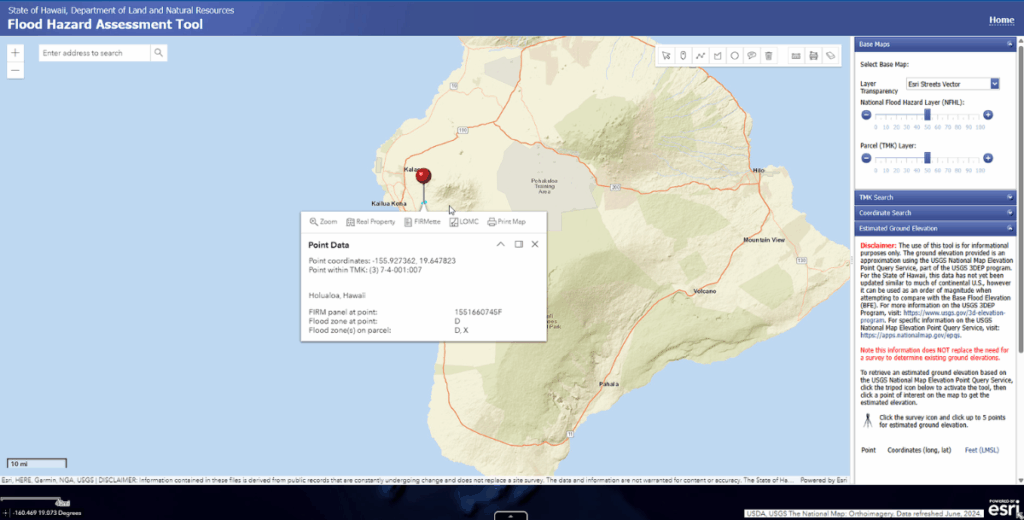

A great tool for determining flood zone classification for Hawaii is via the State of Hawaii, Department of Land and Natural Resources Flood Assessment Tool. Bring up the tool, position your mouse over the area in question and you’ll see the Zone.

How SFHAs Affect Permitting and Building

Counties often require Elevation Certificates and special construction standards within these areas. That could mean:

-

Raising the lowest floor of a structure above the Base Flood Elevation (BFE)

-

Reinforcing foundations

-

Limiting certain types of improvements or additions

Translation? Budget and design flexibility get tighter in these zones.

When Flood Insurance Is Required — and When It’s Just Smart

Flood insurance isn’t just about meeting a lender’s checklist. In Hawaii, it’s also about protecting your investment in an environment that throws surprises — from torrential rains to sea level changes and infrastructure limitations.

Mandatory vs. Optional Coverage

-

Required if your home is in a high-risk flood zone and financed through a federally regulated lender.

-

Optional if you’re in a moderate- to low-risk zone or you own your home outright.

But here’s the catch:

More than 25% of NFIP claims come from outside high-risk zones.

Translation? You could be in Zone X and still get hit with thousands in water damage during one bad storm.

Private Flood Insurance in 2025

As of this year, Hawaii continues to see growth in private flood insurance options, many of which are now competitive with — or even cheaper than — NFIP policies. These often cover higher-value properties better and include coverage exclusions NFIP doesn’t touch.

Monthly Premium Range in 2025

-

NFIP Average: $800–$1,400/year depending on zone and home value

-

Private Market: Starting as low as $500/year for low-risk areas

Amala Place flooded at Kanaha Beach, Maui, Hawaii. March 23, 2004. Image by http://www.starrenvironmental.com/

What’s New in 2025: FEMA Map Revisions & Local Updates

Flood zone maps are not static — especially not in Hawaii, where coastlines, rainfall patterns, and development trends are constantly shifting. In 2025, FEMA and local governments are continuing to revise and refine flood zone boundaries based on updated data.

FEMA Map Updates Rolling Out by County

As of late 2025, FEMA is in various stages of revising FIRMs (Flood Insurance Rate Maps) across the state. Highlights include:

-

Maui County: Major remapping near Kihei and Lahaina due to updated coastal erosion data post-2023 wildfires.

-

Big Island: More refined mapping in Hilo and Kona reflecting increased stormwater impact modeling.

-

Oahu: Ongoing floodplain analysis around Pearl City and parts of the North Shore.

Why This Matters for Homeowners

If your property moves into a high-risk zone due to a map update, you may:

-

Be required to start carrying flood insurance

-

Need an elevation certificate to contest the new designation

-

See changes in NFIP or private market premium quotes

Tip: If you’re currently outside a flood zone, consider locking in a low-rate policy now — it can be grandfathered in if your zone changes later.

Final Thoughts: Flood Risk Awareness as a Hawaii Homeowner

Flood risk in Hawaii isn’t something to ignore — but it also isn’t something to fear if you know how to navigate it. Maps, zones, and insurance rules may shift, but the core mindset stays the same: protect what you’ve got, and plan for what might come.

Whether you’re buying your first home here or just reassessing your current setup, take a little time to:

-

Check your address on the FEMA and county maps

-

Understand your current zone and what it actually means

-

Weigh the costs and benefits of flood insurance, even if it’s not “required”

In a place as naturally dynamic as Hawaii, staying informed isn’t just smart — it’s part of living well.

Summary

-

Use FEMA’s and your county’s GIS tools to check flood zones

-

Understand your zone type (AE, VE, X, etc.) and its insurance implications

-

Risk Rating 2.0 means more customized NFIP pricing in 2025

-

Monthly flood insurance payments are now widely available

-

Flood map changes in 2025 could impact your zone and insurance status

-

Optional flood insurance can be a smart move, even in “low-risk” areas